Bringing Profitable Wholesale Economics Back to the Media Industry in the Streaming Era

July 14, 2026

“Streaming” has become a ubiquitous catch-all term for all types of web-delivered video. But as traditional linear television declines, the line between streaming and television is fading; we’re on the cusp of a generation that may know no such distinction at all.

While this consumer terminology has centered around how video is distributed and delivered, from the business perspective, streaming has had another meaning. It’s been synonymous with direct-to-consumer. Sure, there’s a technical element to the delivery technology, but what’s been truly transformative to the media business is the relationship with the customer.

In the past, the customer only had a relationship with the MVPDs. Viewers recognized brands like Time Warner, Disney, and NBC Universal, but had no direct transactions with them. In this business model, Netflix was a pioneer, proving to all the big media players that these direct customer relationships weren’t just possible within the video entertainment space, they could be quite lucrative. As the high price of traditional pay TV turned consumers into cord-cutters, this was beginning to look like the superior strategy.

Now, about a decade in to that transition, streaming services are just now starting to put the first bit of black on the balance sheet after years as money pits. A strange contradiction has emerged: more clearly than ever, the future belongs to streaming, but none of these major streaming services, each one a worthy rival to Netflix on paper, has enjoyed great financial success.

Built Different: Netflix versus Legacy Media

Since its inception, and the early days when it was renting DVDs by mail, Netflix’s designs were right in its name: delivering flicks via the net. At a fundamental level, the company’s business as well as its technology were built around doing this. That’s a stark contrast to the legacy media companies against which it would go on to compete. At great expense, they were able to duplicate Netflix’s technology, but they did so at the expense of the business model they had perfected.

Pay TV channels were the cash cows that they were precisely because of wholesale economics. A single cable or satellite TV provider served millions of homes, so one single deal created an enormous and dependable revenue stream. With channels bundled together and foisted upon customers who had no option to refuse even the ones they didn’t want, the big media brands earned themselves billions in revenue on a monthly basis.

This approach kept media companies focused. They had one job: make great content. That would matter far more than anything a negotiator at the table with the TV providers could do. Comcast and DirecTV had to make a deal with Disney, because they’d face a customer revolt if ESPN disappeared from their TV dial. To this day, that’s what these brands are known for. Disney is synonymous with children’s programming and princess movies, Time Warner and HBO carry the cachet of prestige TV, Paramount and Warner Bros. are movie theater mainstays.

On content, Hollywood had every advantage against Netflix. The original SVOD service had to spend massively on original content to compete on that level. But the real battle wasn’t in media critic columns, it was business. Netflix had been built from the ground up around direct-to-consumer economics. For legacy media companies, that shift meant billions in investment, followed by high customer-acquisition costs and churn. They’d effectively traded a high-margin business where they had a competitive advantage for a battlefield where they’d have to fight for every subscriber.

Wholesale for the Streaming Era

The shift from wholesale to direct-to-consumer “retail” economics has been one of the main drags on the profitability of the media industry as it has shifted in to the streaming era. Chasing customers one by one just isn’t efficient, and it has required otherwise successful businesses to add new whole new operations. Rather than remain specialized in producing content, these firms have had to become tech companies and market themselves to customers in a whole new way.

It’s been an expensive undertaking that hasn’t yet been fruitful, and that’s for some of the biggest companies in the industry that had the resources to attempt it at all. For smaller firms that don’t have billions in existing pay TV revenues, the decline in traditional TV and the consumer shift to streaming has created an existential crisis with no good solution in sight.

Despite the vastly different circumstances that large and small media companies confront, and the difference in resources between them, they both share the same need with the same solution: to get out of the tech business and stop paying to acquire the same customer time and again.

The answer is a return to a wholesale approach to media. While it’s not possible to turn back the clock on the past ten years of consumer trends, it’s not too late to start building towards a future that works.

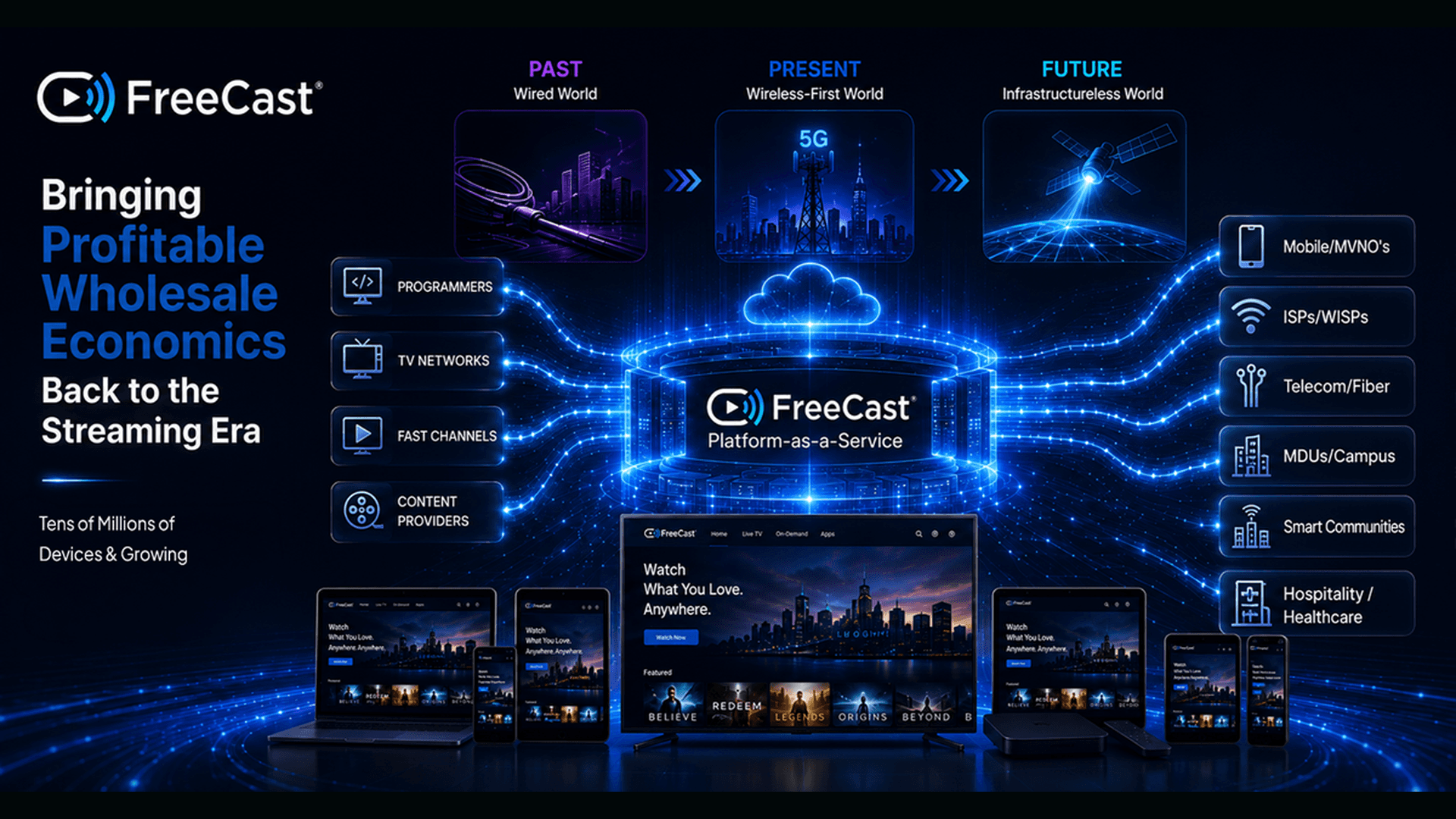

The best news is that FreeCast has already built the infrastructure and now offers it as a Platform-as-a-Service. The company has spent more than 10 years and over $50 million assembling all the myriad technologies and vendors that it takes to become a streaming company, combining them in a plug-and-play solution for other companies.

Profitable Streaming that Scales

Becoming a streaming company has been an expensive proposition, largely because so many large companies duplicated their costs. While there were always multiple cable TV providers, you never had a dozen different companies building infrastructure in the same areas, those firms were notorious for their regional monopolies. But that’s precisely what happened with streaming infrastructure: everybody built their own means to reach the exact same customers, on the same devices, in the same way.

This not only put infrastructure costs on every balance sheet rather than consolidating them, it created a headache for consumers who now have to juggle far too many streaming apps.

FreeCast’s PaaS is designed as a common infrastructure that solves both problems at once, it consolidates content in one place for consumers while creating a single distribution medium so that every programmer doesn’t have to invest in building their own.

This solution was designed to scale, able to accommodate the smallest of programmers all the way up to multi-billion dollar media giants. It also makes economic sense at both levels; it’s low-cost to get started and begins generating revenue almost immediately. FreeCast shares its revenue, so it makes money when its partners make money, keeping the company neutral and aligned with its programmers. The service is designed to be revenue-positive for partners almost immediately, whether they’re a small channel with a niche or regional audience, or a large programmer that reaches millions.

By operating as a platform-as-a-Service, FreeCast opens the door to a variety of other commercial opportunities for other firms that are not programmers. Distribution partners share in many of the same benefits of revenue sharing and consolidation of technology and infrastructure investment.

Multi-family housing, the hospitality and healthcare industries, device manufacturers, telcos and bandwidth providers, and membership organizations across the globe can use FreeCast to deploy a video service that generates revenue and solves a key consumer pain point by taking the complexity out of streaming. This in turn brings large numbers of users onto the platform with minimal customer acquisition costs. Like the old days of cable TV, one a single deal can bring in thousands or millions of users at once.

Pairing these solutions together isn’t coincidental, the way FreeCast serves both programmers and distributors is a necessary piece of its success in tackling the unique challenges that face each of them. While so many media companies were aiming to build another Netflix, FreeCast was hard at work on a thoughtful, long-term solution that the media industry needs.